Friendly fraud

Friendly fraud

Blog

Patterns of friendly fraud and how they impact Merchants and Issuing Banks

Patterns of friendly fraud and how they impact Merchants and Issuing Banks

Patterns of friendly fraud and how they impact Merchants and Issuing Banks

Friendly fraud is first-party fraud; occurring when consumers abuse business policies to receive fraudulent refunds or receive goods/services with a promise to pay later, and then disappear without doing so.

Lerato Matsio

Lerato Matsio

17 Jun 2024

17 Jun 2024

Over the years, friendly fraud has been steadily increasing owing to activity by professional fraud syndicates and ‘regular’ consumers.

In 2023, 42% of GenZ consumers admitted to intentionally engaging in friendly fraud, along with 22% of Millennials and 10% Gen X.

19% of these fraudsters shared that they did not find what they did to be morally wrong.

In this article we discuss 6 patterns of friendly fraud that play out across the payments ecosystem; impacting merchants, marketplaces, issuing banks and lenders.

1. Multiple identities (sometimes synthetic) used to exploit the purchase limits set by merchants or use loyalty points fraudulently

It is commonplace with brands and retailers to apply purchase limits or loyalty point caps for individual consumers. Friendly fraudsters use multiple identities to deceive merchants and purchase higher quantities of goods than would be otherwise permitted. Goods are then resold on marketplaces at a higher value than store price. Similarly, friendly fraudsters use multiple accounts (e.g., opened through different emails) to exploit loyalty benefits.

2. Pay-later fraud or credit fraud

Ecommerce merchants are increasingly offering consumers flexible payment options, including various pay later schemes such as ‘pay-after-delivery’ and ‘pay-by-instalment’. As a result, the BNPL market has grown with even banks seeking to expand their propositions to offer pay-later products in the market.

Friendly fraudsters may abuse these credit offerings, to receive goods on credit and then disappear without repayment. This pay-later fraud is not isolated to only ecommerce merchants with BNPL offerings in their checkout flows.

It also impacts telecom companies offering, for example, smart phones on mobile plans contracted over 24 months. Friendly fraudsters may visit an outlet to take a mobile contract requiring repayment over time. Shortly after, they may sell the device for cash, without repaying the contract and then re-appear at a different outlet to take out another contract and repeat the cycle.

Consumer credit risk assessments, through a lens of friendly fraud, is essential for all businesses facing a consumer credit risk.

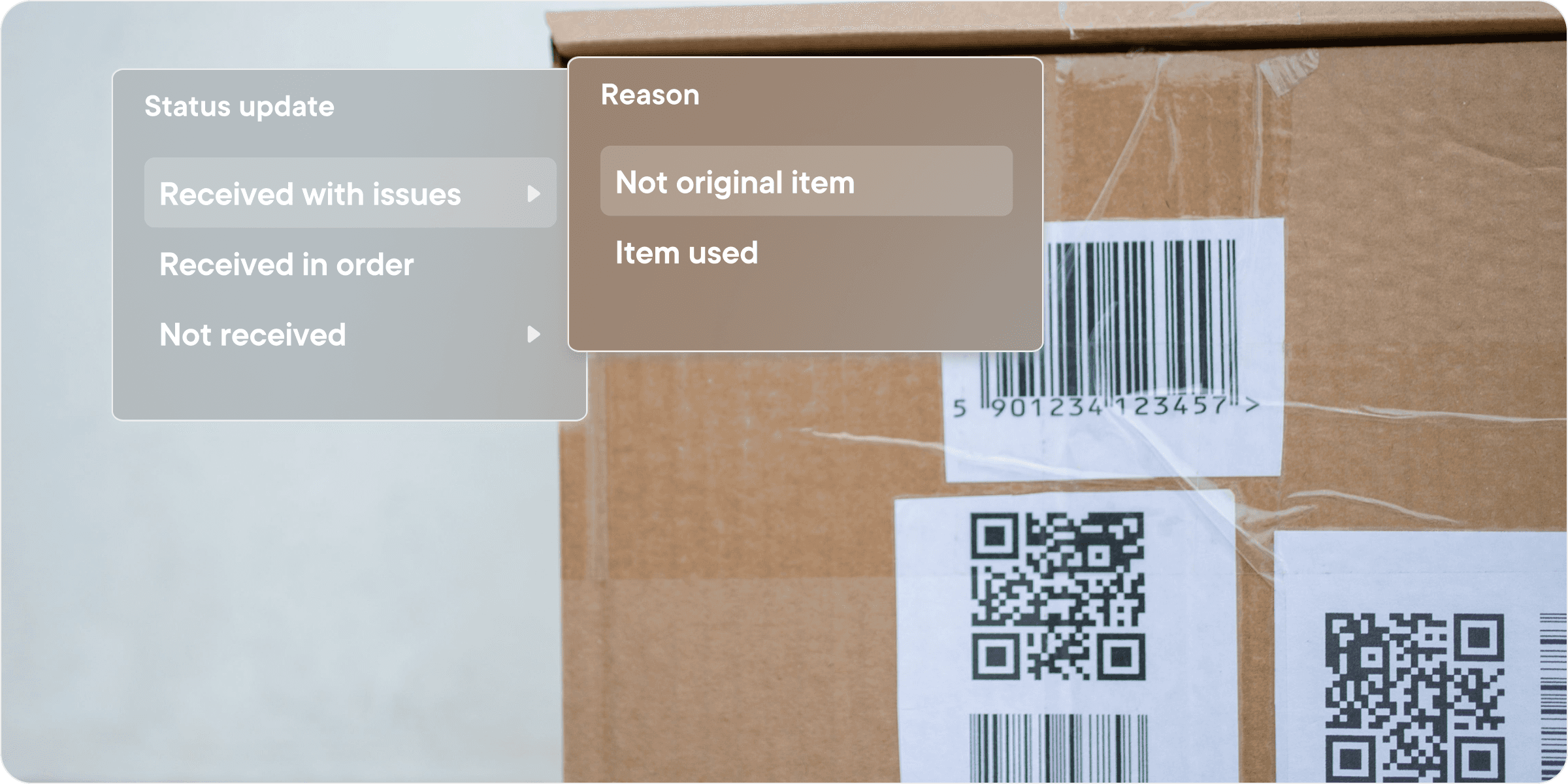

3. Claims of delivery-not-done

Ecommerce merchants are often pushed to provide refunds to consumers claiming to not have received their deliveries, even though they have. This common form of friendly fraud has fortunately received ample attention resulting in the existence of various point-solutions providing irrefutable 'proof of delivery'. Some examples include using video footage by delivery partners to capture physical evidence of successful delivery and OTPs deployed in our favourite food delivery apps.

Given the frequent occurrence of delivery-not-done fraud, specialised insurance offerings providing cover against lost-in-transit goods are also gaining traction in the market.

Personalised consumer fraud risk intelligence, enabling the differentiation between trusted consumers and friendly fraudsters, would enable merchants to optimise the application of ‘proof of delivery’ solutions. It would also enable more accurate underwriting for insurers and empower merchants to transfer the cost for insurance to friendly fraudsters, whilst offering this cover to trusted customers at no extra charge.

If a friendly fraudster is unable to get away with claiming that parcels have not been delivered, to receive a fraudulent refund, they will attempt to send it back to receive a refund.

There are 3 variations of returns fraud currently in play.

4. Faking the returns of goods

Fraudsters will send back a box, holding miscellaneous items that weigh the same as the original, often high value item. Large merchants processing high volumes of returns typically operate streamlined operations that weigh parcels to verify returned parcels, and process refunds once the parcel is scanned in the warehouse.

It is this very loophole used by fraudsters to defraud merchants who do not inspect each returned item before processing a refund.

Embedding personalised consumer fraud risk intelligence into workflows will enable merchants to apply dynamic and differentiated rules to consumer returns, for example, automated refund decisioning for trusted consumers, whilst requiring thorough inspections for items returned by high risk consumers.

5. Modifying returns labels, resulting in lost returns

As an alternative to faking the returns, friendly fraudsters modify returns labels so that returned parcels never quite arrive at the warehouse. If your business experiences a high volume of lost returns, you may be experiencing friendly fraud. When these items are lost with a successfully scanned returns label, merchants are compelled to process the consumer refund.

6. Returning used goods

Most millennials will remember watching “Confessions of a Shopaholic”, and seeing Isla Fischer’s character purchasing clothing, wearing them with the tag still on, only to return it for a refund. Wardrobing, is still a hot trend affecting even online merchants, with effects beyond goods that cannot be resold. Wardrobing places a burden on operations, from logistics to warehouse operations.

Some consumers purchase many items, keep some and return most. Even if the consumer in question has not worn the items, this practice has a cost for the merchant.

Merchants can optimise operating costs by identifying which consumers exhibit these behaviours, and limiting the extent to which they do it.

Trudenty not only provides personalised consumer fraud risk intelligence - we also work with your team to define how it can be integrated into workflows to unlock benefits across the business for bottom line impact.

7. Chargeback fraud

An article about first party fraud would be incomplete without a mention of chargeback fraud.

The market has various chargeback guarantee solutions which transfer the liability for chargeback fraud from merchants to issuing banks, then assist with the dispute resolutions associated with these chargeback claims. Solutions also exist to prevent erroneous chargebacks requested by consumer’s who have forgotten that they have made legitimate charges.

Considering everything we’ve just discussed about patterns of friendly fraud, and the clear intentionality behind each of them: Is it possible that chargeback fraud is more intentional than once thought?

The truth is; consumers engaging in one kind of friendly fraud are more likely to engage in others. A business is better off understanding this and taking a holistic approach.

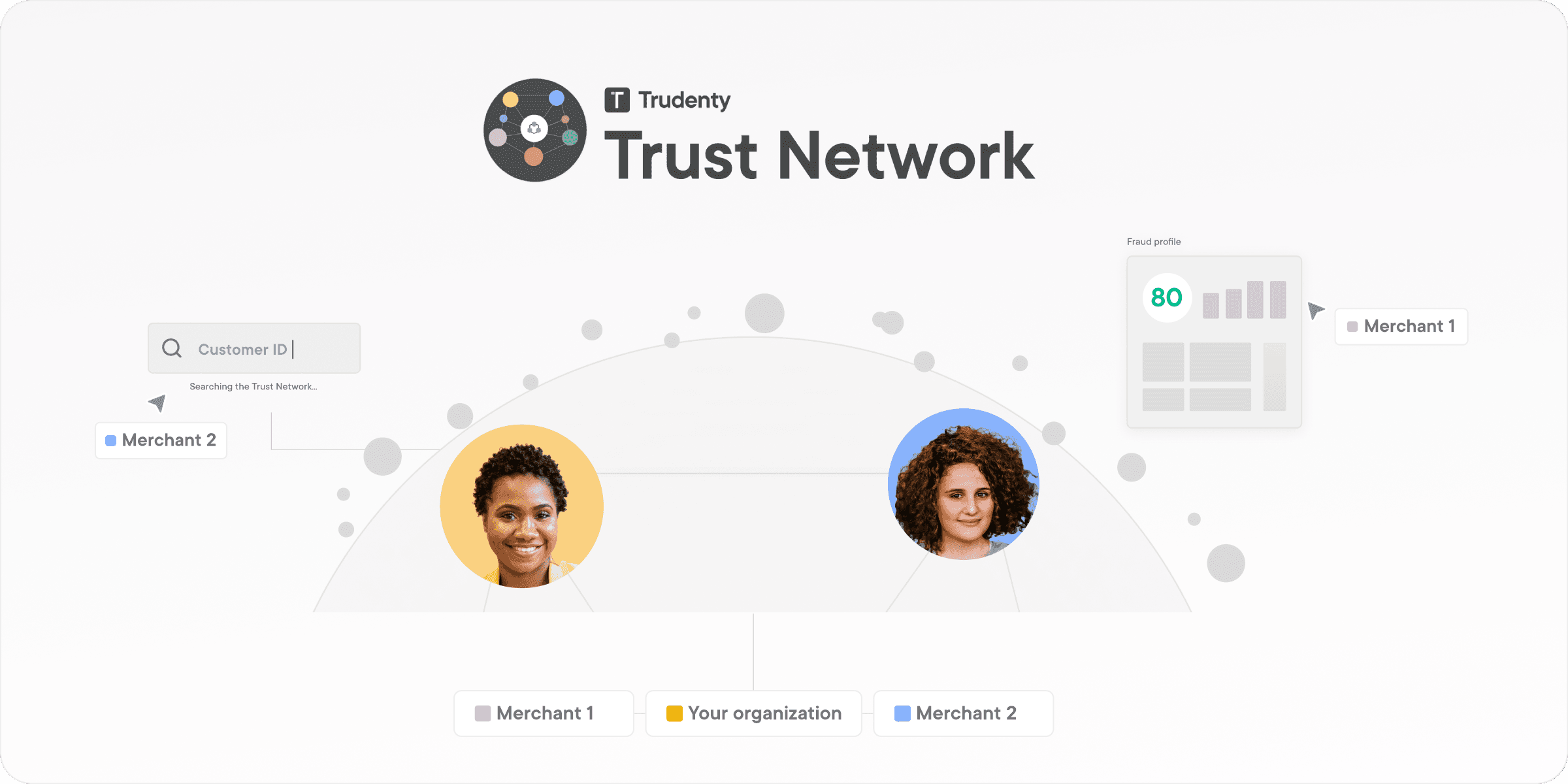

The Trudenty Trust Network provides personalised, consumer fraud risk intelligence enabling merchants and issuing banks to identify friendly fraudsters.

Contact us to discuss first-party fraud in your business, and how you could prevent it.

Over the years, friendly fraud has been steadily increasing owing to activity by professional fraud syndicates and ‘regular’ consumers.

In 2023, 42% of GenZ consumers admitted to intentionally engaging in friendly fraud, along with 22% of Millennials and 10% Gen X.

19% of these fraudsters shared that they did not find what they did to be morally wrong.

In this article we discuss 6 patterns of friendly fraud that play out across the payments ecosystem; impacting merchants, marketplaces, issuing banks and lenders.

1. Multiple identities (sometimes synthetic) used to exploit the purchase limits set by merchants or use loyalty points fraudulently

It is commonplace with brands and retailers to apply purchase limits or loyalty point caps for individual consumers. Friendly fraudsters use multiple identities to deceive merchants and purchase higher quantities of goods than would be otherwise permitted. Goods are then resold on marketplaces at a higher value than store price. Similarly, friendly fraudsters use multiple accounts (e.g., opened through different emails) to exploit loyalty benefits.

2. Pay-later fraud or credit fraud

Ecommerce merchants are increasingly offering consumers flexible payment options, including various pay later schemes such as ‘pay-after-delivery’ and ‘pay-by-instalment’. As a result, the BNPL market has grown with even banks seeking to expand their propositions to offer pay-later products in the market.

Friendly fraudsters may abuse these credit offerings, to receive goods on credit and then disappear without repayment. This pay-later fraud is not isolated to only ecommerce merchants with BNPL offerings in their checkout flows.

It also impacts telecom companies offering, for example, smart phones on mobile plans contracted over 24 months. Friendly fraudsters may visit an outlet to take a mobile contract requiring repayment over time. Shortly after, they may sell the device for cash, without repaying the contract and then re-appear at a different outlet to take out another contract and repeat the cycle.

Consumer credit risk assessments, through a lens of friendly fraud, is essential for all businesses facing a consumer credit risk.

3. Claims of delivery-not-done

Ecommerce merchants are often pushed to provide refunds to consumers claiming to not have received their deliveries, even though they have. This common form of friendly fraud has fortunately received ample attention resulting in the existence of various point-solutions providing irrefutable 'proof of delivery'. Some examples include using video footage by delivery partners to capture physical evidence of successful delivery and OTPs deployed in our favourite food delivery apps.

Given the frequent occurrence of delivery-not-done fraud, specialised insurance offerings providing cover against lost-in-transit goods are also gaining traction in the market.

Personalised consumer fraud risk intelligence, enabling the differentiation between trusted consumers and friendly fraudsters, would enable merchants to optimise the application of ‘proof of delivery’ solutions. It would also enable more accurate underwriting for insurers and empower merchants to transfer the cost for insurance to friendly fraudsters, whilst offering this cover to trusted customers at no extra charge.

If a friendly fraudster is unable to get away with claiming that parcels have not been delivered, to receive a fraudulent refund, they will attempt to send it back to receive a refund.

There are 3 variations of returns fraud currently in play.

4. Faking the returns of goods

Fraudsters will send back a box, holding miscellaneous items that weigh the same as the original, often high value item. Large merchants processing high volumes of returns typically operate streamlined operations that weigh parcels to verify returned parcels, and process refunds once the parcel is scanned in the warehouse.

It is this very loophole used by fraudsters to defraud merchants who do not inspect each returned item before processing a refund.

Embedding personalised consumer fraud risk intelligence into workflows will enable merchants to apply dynamic and differentiated rules to consumer returns, for example, automated refund decisioning for trusted consumers, whilst requiring thorough inspections for items returned by high risk consumers.

5. Modifying returns labels, resulting in lost returns

As an alternative to faking the returns, friendly fraudsters modify returns labels so that returned parcels never quite arrive at the warehouse. If your business experiences a high volume of lost returns, you may be experiencing friendly fraud. When these items are lost with a successfully scanned returns label, merchants are compelled to process the consumer refund.

6. Returning used goods

Most millennials will remember watching “Confessions of a Shopaholic”, and seeing Isla Fischer’s character purchasing clothing, wearing them with the tag still on, only to return it for a refund. Wardrobing, is still a hot trend affecting even online merchants, with effects beyond goods that cannot be resold. Wardrobing places a burden on operations, from logistics to warehouse operations.

Some consumers purchase many items, keep some and return most. Even if the consumer in question has not worn the items, this practice has a cost for the merchant.

Merchants can optimise operating costs by identifying which consumers exhibit these behaviours, and limiting the extent to which they do it.

Trudenty not only provides personalised consumer fraud risk intelligence - we also work with your team to define how it can be integrated into workflows to unlock benefits across the business for bottom line impact.

7. Chargeback fraud

An article about first party fraud would be incomplete without a mention of chargeback fraud.

The market has various chargeback guarantee solutions which transfer the liability for chargeback fraud from merchants to issuing banks, then assist with the dispute resolutions associated with these chargeback claims. Solutions also exist to prevent erroneous chargebacks requested by consumer’s who have forgotten that they have made legitimate charges.

Considering everything we’ve just discussed about patterns of friendly fraud, and the clear intentionality behind each of them: Is it possible that chargeback fraud is more intentional than once thought?

The truth is; consumers engaging in one kind of friendly fraud are more likely to engage in others. A business is better off understanding this and taking a holistic approach.

The Trudenty Trust Network provides personalised, consumer fraud risk intelligence enabling merchants and issuing banks to identify friendly fraudsters.

Contact us to discuss first-party fraud in your business, and how you could prevent it.

Trudenty

The Trust Network enables merchants, acquirers and issuers to collaborate and share consumer fraud risk intelligence in a regulatory compliant manner.

Subscribe to our newsletter

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

Follow us

© Copyright 2025. All Rights Reserved.

Trudenty

The network enables merchant networks to collaborate and share consumer intelligence in a regulatory compliant manner. Leverage our next-gen machine-learning powered smart contract algorithms to distill consumer insights to solve merchant pain points.

Subscribe to our newsletter

Follow us

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

© Copyright 2025. All Rights Reserved.

Trudenty

The Trust Network enables merchants, acquirers and issuers to collaborate and share consumer fraud risk intelligence in a regulatory compliant manner.

Subscribe to our newsletter

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

Follow us

© Copyright 2025. All Rights Reserved.

Book a demo