Your Friendly Fraud Blueprint

Your Friendly Fraud Blueprint

Blog

Understanding And Preventing Friendly Fraud

Understanding And Preventing Friendly Fraud

Understanding And Preventing Friendly Fraud

First-party fraud, often called friendly fraud, is a growing challenge in ecommerce, including for Shopify merchants.

Giulia Sale

Giulia Sale

4 Nov 2024

4 Nov 2024

This type of fraud occurs when a consumer abuses a business policy or regulation to receive a fraudulent payout, often a refund.You might have heard stories of customers who purchase items and dispute the charges through their bank or credit card provider, often claiming they never received the item or that the product didn’t meet expectations.

Although labelled "friendly," this fraud costs ecommerce businesses a lot of money, hours, and stress.

Why is it called friendly fraud?

Strictly speaking, friendly fraud is ‘first-party fraud’.

Referring to it as friendly fraud emphasises that it is committed by a merchant’s own customers, people who may have an established relationship with the business, and not only by organised fraud syndicates.

We’re witnessing a shift in societal psychology around fraud, with a rise in TikTok trends where consumers share ‘life hacks’ that lead to fraud.

About friendly fraud

If you are reading this document, you are most likely to be experiencing first-party fraud.

Do not worry, your business is not the only one and this issue is more common than you might think.

Recent studies reveal just how significant this issue has become:

42% of Gen Z, 22% of millennials and 10% of Gen X consumers admit to engaging in friendly fraud.

19% of these consumers have shared that they see no moral issue with engaging in friendly fraud

This behaviour has contributed to an astounding $100 billion in annual losses due to friendly fraud in 2023, and this figure is already up by 25-30% for 2024.

In 2024, a survey of 1100 Shopify merchants revealed that 63% of them were experiencing more first-party fraud than they had a year ago.

What is friendly fraud?

Friendly fraud occurs when a legitimate customer or someone appearing like a legitimate consumer misrepresents their intentions or the circumstances around a purchase to gain a financial advantage or avoid payment.

Here are the main types of first-party fraud, along with explanations.

Item Not Received (INR)

Explanation: The customer claims they never received the item, even though tracking information may show successful delivery. This type of fraud can be difficult to dispute, especially if there’s no signature required on delivery.

Example: A customer orders a product online, receives it, but then contacts the merchant or their credit card issuer to claim it never arrived, asking for a replacement or refund.

Item Not Receive can also look as:

Interception Fraud

Explanation: Interception fraud involves a customer placing an order and then redirecting the shipment to a different address after it’s en route, often to claim that they never received the item at the original address.

Example: A customer places an order and then contacts the shipping company to reroute it to a new address, then disputes the charge with the merchant, claiming it never arrived.

Return & Refund Fraud

Explanation: In return & refund fraud, the customer returns an item or requests a refund with the intent to deceive. This could include returning a used or damaged item, returning an item in a different condition than it was sold, or asking for a refund without returning the original item.

Example: A customer purchases a designer handbag, uses it for an event, and then returns it claiming dissatisfaction or a defect, though it’s used and no longer new.

Chargeback Fraud

Explanation: This happens when a customer makes a legitimate purchase, receives the product or service, but later disputes the charge with their bank or credit card provider. They might claim they never received the product, that it was defective, or that they didn’t authorize the transaction, leading to a chargeback where the merchant loses both the sale and the product.

Example: A customer orders a luxury item, receives it, and then disputes the charge with their bank, claiming it was unauthorized.

Wardrobing (Free Renting)

Explanation: Wardrobing is a form of return fraud where the customer "rents" an item by purchasing it, using it temporarily and then returning it for a full refund. This type of fraud is especially common with clothing and high-end electronics.

Example: A shopper buys an expensive dress, wears it to an event with tags hidden, and then returns it afterwards, claiming it wasn’t the right fit.

Identity Misrepresentation

Explanation: Here, a customer uses real information but may slightly alter their identity or billing details to bypass risk detection systems or secure financing or credit they don’t intend to repay.

Example: A shopper purchases high-end electronics using their real information but slightly alters their billing address to circumvent credit checks, then fails to make payments.

Promotion Abuse

Explanation: This type of fraud occurs when customers repeatedly take advantage of promotional offers by creating multiple accounts, using different emails, or slightly altering personal information to qualify as a “new customer.”

Example: A customer creates multiple email addresses to repeatedly use a “first-time buyer” discount or other limited-time offers.

Service / Policy Abuse

Explanation: Service / Policy abuse involves customers repeatedly taking advantage of a store’s lenient policies, such as no-questions-asked returns or satisfaction guarantees, to benefit financially or to avoid spending.

Example: A shopper purchases an item knowing they’ll likely return it if they find a better price elsewhere, treating the store as a risk-free "backup" option.

Service / Policy abuse can also look like:

Unwarranted Warranties

Explanation: Customers may buy products and repeatedly claim issues to abuse warranty programs, seeking excessive free repairs or replacements over the product’s lifetime.

Example: A customer claims multiple "defects" in a smartphone, seeking free replacements for issues that may not actually exist, especially toward the end of a warranty period.

The rise of first party-fraud

Why is friendly fraud hard to tackle?

With the convenience of online shopping, there are more avenues for consumers to commit friendly fraud, often without realizing its impact.Here are some reasons why:

Misuse of dispute processes: Banks and payment processors offer simple dispute options, sometimes favouring customers over merchants.

Changing consumers’ attitude: Younger generations may see “testing” policies as a way to avoid the costs of trying new products or as a low-risk way to “borrow” items.

High-return seasons: Peak shopping events like Black Friday lead to a surge in returns and refund requests, making it hard for merchants to assess each claim’s validity.

Monitoring gaps in traditional fraud detection: Most fraud prevention tools focus on digital transaction monitoring, but friendly fraud often occurs in real-world interactions or human-driven processes.

Isolated fraud prevention processes: Traditional fraud tools rely on data from one company, but friendly fraud unfolds across multiple businesses, requiring a collaborative approach. E.g., A customer might request a refund once or twice if they genuinely didn’t like the product. But if a customer repeatedly requests refunds from many different stores, it's likely they're committing fraud.

Abuse of consumer protections: Financial institutions have put in place regulations to protect consumers from fraudulent businesses. However, consumers have realised how much they are protected, to the point that they are taking advantage of those regulations. On the other hand, not many protection processes are being put in place to protect businesses from friendly fraudsters.

The financial toll on Shopify merchants

First-party fraud drains resources in multiple ways:

Direct financial losses: Merchants lose revenue and inventory each time a chargeback is issued.

Increased operational costs: Processing disputes, reviewing claims, and handling returns require time and manpower.

Higher chargeback ratios: Excessive chargebacks can impact payment processing rates or even lead to account suspensions.

Loss of time: On average, Shopify merchants spend 1 hour per refund or return claim trying to dispute the validity of the claim, being in communication with the consumer and delivery partner, and keeping up with payment processes.

All Or nothing approach: Because merchants are trying to protect themselves from fraud, they take preventative approaches and risk delivering bad customer service to loyal consumers, hence decreasing brand loyalty and returning customers.

5 ways to reduce fraud

Depending on the types of friendly fraud your business encounters, some or all of these steps may be a good starting point to prevent friendly fraud before it happens.

1. Strengthen your return policy

Why: Clear, firm return policies set customer expectations and reduce refund abuse.

How: Use Shopify’s Policy Generator to create detailed refund conditions, such as requiring items to be returned in original condition within a specific time frame.

Tip: Consider including restocking fees for certain items to dissuade casual returns.

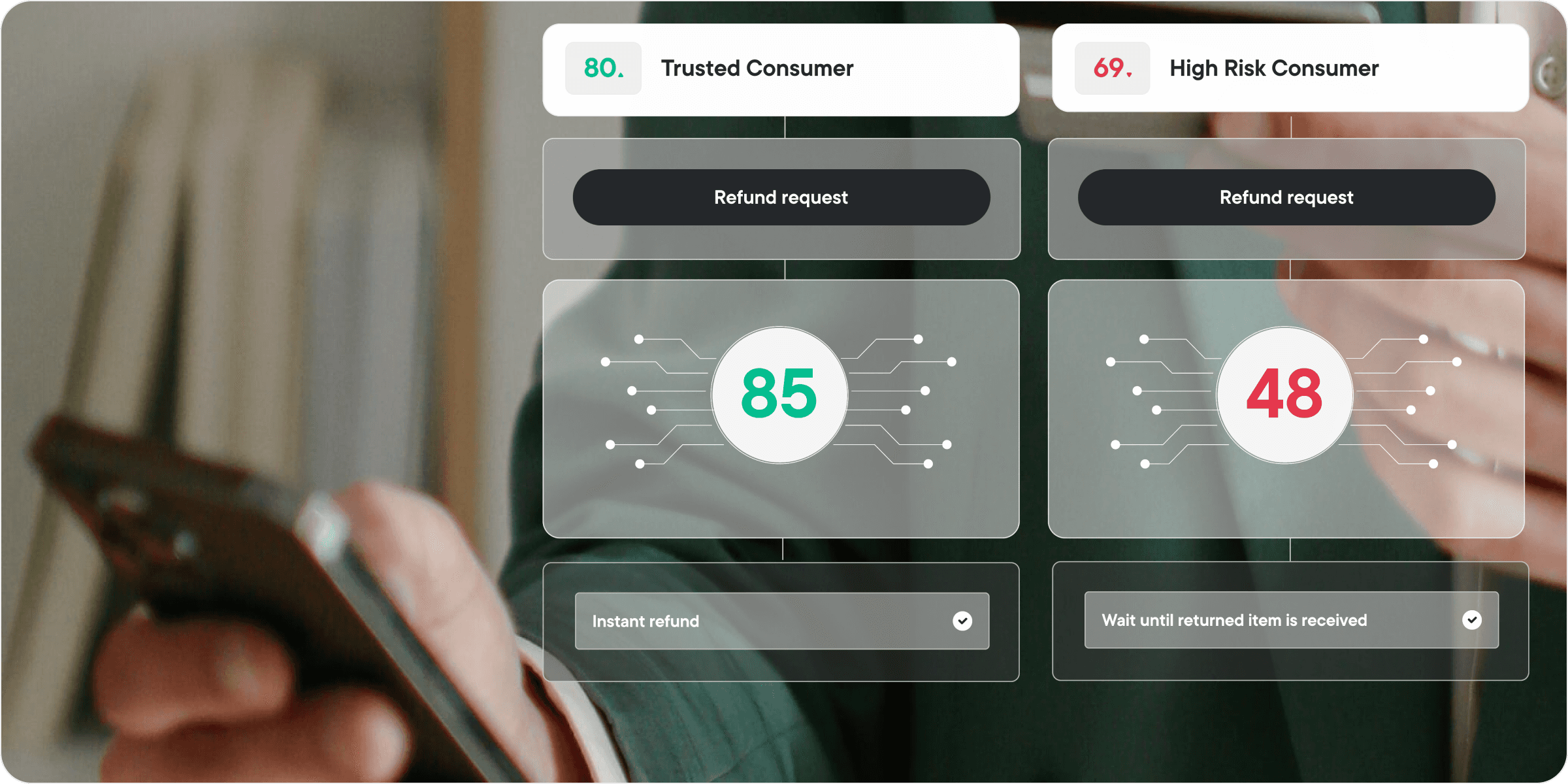

2. Use fraud prevention tools

Why: Automated fraud prevention tools can flag suspicious activity before the sale is completed.

How: Implement the Trudenty Consumer Trust Network’s personalised consumer fraud risk intelligence to identify repeat offenders and track behaviours associated with friendly fraud. Shopify's own Fraud Analysis can complement this, highlighting orders with red flags like mismatched addresses.

Tip: Set up custom alerts for orders with risky characteristics, like high-ticket items or express shipping.

3. Implement strong authentication methods like 3DSecure

Why: Fraudsters are less likely to target stores with robust verification measures.

How: In the case of chargeback fraud, 3DSecure typically shifts responsibility and liability to the consumer’s bank where proper authentication has not occurred.

Tip: Encourage secure payment options like Apple Pay, which adds extra layers of authentication.

4. Leverage post-sale communication

Why: Frequent and clear communication reduces misunderstandings and preempts disputes, including billing statements.

How: Use email reminders for delivery confirmations and follow-up messages inviting feedback. Tools like Klaviyo can automate this process.

Tip: Provide clear support links in follow-ups to offer help, reducing the chance of direct disputes.

5. Collaborate with other stakeholders in the ecommerce ecosystem

Why: Collaborating with others will allow you to look at a customer's holistic history.

How: Collaborating through data-sharing with other merchants to identify friendly fraudsters across the ecosystem, and build a safe environment for all. Networks like Trudenty's Consumer Trust Network can help with this.

Tip: Join online Shopify communities, or invest in online networks to safely share insights with other merchants.

Protect your ecommerce from friendly fraud

Friendly fraud is a growing concern, but with proactive measures and the right tools, you can safeguard your store and minimise losses.

As Black Friday and the holiday seasons approach, using strategies and tools like Trudenty can help ensure you’re capturing sales without sacrificing profits.

We are here to help!

Book a free 20-minute consultation with an expert to receive a more personalised approach towards protecting your Shopify Store from friendly fraud.

Stop friendly fraud before it happens

Stop friendly fraud before it happens with Trudenty’s Consumer Trust Network - reduce losses owing to friendly fraud, save time, and identify trustworthy customers.

Trudenty’s Consumer Trust Network integrates with your Shopify store to automatically detect and manage fraudsters while enabling personalised experiences that build trust and loyalty.

Start quickly and optimise continuously with built-in fraud intelligence, easy-to-use tools, and real-time insights—all from a single dashboard embedded directly into your Shopify Admin Dashboard.

This type of fraud occurs when a consumer abuses a business policy or regulation to receive a fraudulent payout, often a refund.You might have heard stories of customers who purchase items and dispute the charges through their bank or credit card provider, often claiming they never received the item or that the product didn’t meet expectations.

Although labelled "friendly," this fraud costs ecommerce businesses a lot of money, hours, and stress.

Why is it called friendly fraud?

Strictly speaking, friendly fraud is ‘first-party fraud’.

Referring to it as friendly fraud emphasises that it is committed by a merchant’s own customers, people who may have an established relationship with the business, and not only by organised fraud syndicates.

We’re witnessing a shift in societal psychology around fraud, with a rise in TikTok trends where consumers share ‘life hacks’ that lead to fraud.

About friendly fraud

If you are reading this document, you are most likely to be experiencing first-party fraud.

Do not worry, your business is not the only one and this issue is more common than you might think.

Recent studies reveal just how significant this issue has become:

42% of Gen Z, 22% of millennials and 10% of Gen X consumers admit to engaging in friendly fraud.

19% of these consumers have shared that they see no moral issue with engaging in friendly fraud

This behaviour has contributed to an astounding $100 billion in annual losses due to friendly fraud in 2023, and this figure is already up by 25-30% for 2024.

In 2024, a survey of 1100 Shopify merchants revealed that 63% of them were experiencing more first-party fraud than they had a year ago.

What is friendly fraud?

Friendly fraud occurs when a legitimate customer or someone appearing like a legitimate consumer misrepresents their intentions or the circumstances around a purchase to gain a financial advantage or avoid payment.

Here are the main types of first-party fraud, along with explanations.

Item Not Received (INR)

Explanation: The customer claims they never received the item, even though tracking information may show successful delivery. This type of fraud can be difficult to dispute, especially if there’s no signature required on delivery.

Example: A customer orders a product online, receives it, but then contacts the merchant or their credit card issuer to claim it never arrived, asking for a replacement or refund.

Item Not Receive can also look as:

Interception Fraud

Explanation: Interception fraud involves a customer placing an order and then redirecting the shipment to a different address after it’s en route, often to claim that they never received the item at the original address.

Example: A customer places an order and then contacts the shipping company to reroute it to a new address, then disputes the charge with the merchant, claiming it never arrived.

Return & Refund Fraud

Explanation: In return & refund fraud, the customer returns an item or requests a refund with the intent to deceive. This could include returning a used or damaged item, returning an item in a different condition than it was sold, or asking for a refund without returning the original item.

Example: A customer purchases a designer handbag, uses it for an event, and then returns it claiming dissatisfaction or a defect, though it’s used and no longer new.

Chargeback Fraud

Explanation: This happens when a customer makes a legitimate purchase, receives the product or service, but later disputes the charge with their bank or credit card provider. They might claim they never received the product, that it was defective, or that they didn’t authorize the transaction, leading to a chargeback where the merchant loses both the sale and the product.

Example: A customer orders a luxury item, receives it, and then disputes the charge with their bank, claiming it was unauthorized.

Wardrobing (Free Renting)

Explanation: Wardrobing is a form of return fraud where the customer "rents" an item by purchasing it, using it temporarily and then returning it for a full refund. This type of fraud is especially common with clothing and high-end electronics.

Example: A shopper buys an expensive dress, wears it to an event with tags hidden, and then returns it afterwards, claiming it wasn’t the right fit.

Identity Misrepresentation

Explanation: Here, a customer uses real information but may slightly alter their identity or billing details to bypass risk detection systems or secure financing or credit they don’t intend to repay.

Example: A shopper purchases high-end electronics using their real information but slightly alters their billing address to circumvent credit checks, then fails to make payments.

Promotion Abuse

Explanation: This type of fraud occurs when customers repeatedly take advantage of promotional offers by creating multiple accounts, using different emails, or slightly altering personal information to qualify as a “new customer.”

Example: A customer creates multiple email addresses to repeatedly use a “first-time buyer” discount or other limited-time offers.

Service / Policy Abuse

Explanation: Service / Policy abuse involves customers repeatedly taking advantage of a store’s lenient policies, such as no-questions-asked returns or satisfaction guarantees, to benefit financially or to avoid spending.

Example: A shopper purchases an item knowing they’ll likely return it if they find a better price elsewhere, treating the store as a risk-free "backup" option.

Service / Policy abuse can also look like:

Unwarranted Warranties

Explanation: Customers may buy products and repeatedly claim issues to abuse warranty programs, seeking excessive free repairs or replacements over the product’s lifetime.

Example: A customer claims multiple "defects" in a smartphone, seeking free replacements for issues that may not actually exist, especially toward the end of a warranty period.

The rise of first party-fraud

Why is friendly fraud hard to tackle?

With the convenience of online shopping, there are more avenues for consumers to commit friendly fraud, often without realizing its impact.Here are some reasons why:

Misuse of dispute processes: Banks and payment processors offer simple dispute options, sometimes favouring customers over merchants.

Changing consumers’ attitude: Younger generations may see “testing” policies as a way to avoid the costs of trying new products or as a low-risk way to “borrow” items.

High-return seasons: Peak shopping events like Black Friday lead to a surge in returns and refund requests, making it hard for merchants to assess each claim’s validity.

Monitoring gaps in traditional fraud detection: Most fraud prevention tools focus on digital transaction monitoring, but friendly fraud often occurs in real-world interactions or human-driven processes.

Isolated fraud prevention processes: Traditional fraud tools rely on data from one company, but friendly fraud unfolds across multiple businesses, requiring a collaborative approach. E.g., A customer might request a refund once or twice if they genuinely didn’t like the product. But if a customer repeatedly requests refunds from many different stores, it's likely they're committing fraud.

Abuse of consumer protections: Financial institutions have put in place regulations to protect consumers from fraudulent businesses. However, consumers have realised how much they are protected, to the point that they are taking advantage of those regulations. On the other hand, not many protection processes are being put in place to protect businesses from friendly fraudsters.

The financial toll on Shopify merchants

First-party fraud drains resources in multiple ways:

Direct financial losses: Merchants lose revenue and inventory each time a chargeback is issued.

Increased operational costs: Processing disputes, reviewing claims, and handling returns require time and manpower.

Higher chargeback ratios: Excessive chargebacks can impact payment processing rates or even lead to account suspensions.

Loss of time: On average, Shopify merchants spend 1 hour per refund or return claim trying to dispute the validity of the claim, being in communication with the consumer and delivery partner, and keeping up with payment processes.

All Or nothing approach: Because merchants are trying to protect themselves from fraud, they take preventative approaches and risk delivering bad customer service to loyal consumers, hence decreasing brand loyalty and returning customers.

5 ways to reduce fraud

Depending on the types of friendly fraud your business encounters, some or all of these steps may be a good starting point to prevent friendly fraud before it happens.

1. Strengthen your return policy

Why: Clear, firm return policies set customer expectations and reduce refund abuse.

How: Use Shopify’s Policy Generator to create detailed refund conditions, such as requiring items to be returned in original condition within a specific time frame.

Tip: Consider including restocking fees for certain items to dissuade casual returns.

2. Use fraud prevention tools

Why: Automated fraud prevention tools can flag suspicious activity before the sale is completed.

How: Implement the Trudenty Consumer Trust Network’s personalised consumer fraud risk intelligence to identify repeat offenders and track behaviours associated with friendly fraud. Shopify's own Fraud Analysis can complement this, highlighting orders with red flags like mismatched addresses.

Tip: Set up custom alerts for orders with risky characteristics, like high-ticket items or express shipping.

3. Implement strong authentication methods like 3DSecure

Why: Fraudsters are less likely to target stores with robust verification measures.

How: In the case of chargeback fraud, 3DSecure typically shifts responsibility and liability to the consumer’s bank where proper authentication has not occurred.

Tip: Encourage secure payment options like Apple Pay, which adds extra layers of authentication.

4. Leverage post-sale communication

Why: Frequent and clear communication reduces misunderstandings and preempts disputes, including billing statements.

How: Use email reminders for delivery confirmations and follow-up messages inviting feedback. Tools like Klaviyo can automate this process.

Tip: Provide clear support links in follow-ups to offer help, reducing the chance of direct disputes.

5. Collaborate with other stakeholders in the ecommerce ecosystem

Why: Collaborating with others will allow you to look at a customer's holistic history.

How: Collaborating through data-sharing with other merchants to identify friendly fraudsters across the ecosystem, and build a safe environment for all. Networks like Trudenty's Consumer Trust Network can help with this.

Tip: Join online Shopify communities, or invest in online networks to safely share insights with other merchants.

Protect your ecommerce from friendly fraud

Friendly fraud is a growing concern, but with proactive measures and the right tools, you can safeguard your store and minimise losses.

As Black Friday and the holiday seasons approach, using strategies and tools like Trudenty can help ensure you’re capturing sales without sacrificing profits.

We are here to help!

Book a free 20-minute consultation with an expert to receive a more personalised approach towards protecting your Shopify Store from friendly fraud.

Stop friendly fraud before it happens

Stop friendly fraud before it happens with Trudenty’s Consumer Trust Network - reduce losses owing to friendly fraud, save time, and identify trustworthy customers.

Trudenty’s Consumer Trust Network integrates with your Shopify store to automatically detect and manage fraudsters while enabling personalised experiences that build trust and loyalty.

Start quickly and optimise continuously with built-in fraud intelligence, easy-to-use tools, and real-time insights—all from a single dashboard embedded directly into your Shopify Admin Dashboard.

Trudenty

The Trust Network enables merchants, acquirers and issuers to collaborate and share consumer fraud risk intelligence in a regulatory compliant manner.

Subscribe to our newsletter

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

Follow us

© Copyright 2025. All Rights Reserved.

Trudenty

The network enables merchant networks to collaborate and share consumer intelligence in a regulatory compliant manner. Leverage our next-gen machine-learning powered smart contract algorithms to distill consumer insights to solve merchant pain points.

Subscribe to our newsletter

Follow us

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

© Copyright 2025. All Rights Reserved.

Trudenty

The Trust Network enables merchants, acquirers and issuers to collaborate and share consumer fraud risk intelligence in a regulatory compliant manner.

Subscribe to our newsletter

Address

Level 18

40 Bank Street

Canary Wharf, UK

E14 5NR

Follow us

© Copyright 2025. All Rights Reserved.

Book a demo